The calls for structural economic transformation in Africa date back to the 1960s when newly independent nations aimed to eliminate poverty through economic diversification, sustained growth, and job creation. This agenda persists today, as Africa continues to face significant developmental challenges.

Pursuing post-independence economic agendas was particularly important because, behind the euphoria of independence, laid significant developmental challenges in several African countries: unskilled labor force, political and institutional fragilities, poor health conditions, rapid population growth, wide income disparities, and the legacy of colonialism and exclusion from the modern world. The establishment of the Organization of African Unity (OAU) in 1963 and the African Development Bank a year later aimed to tackle these other challenges in a more coordinated and impactful manner. The African Union, successor of the OAU, developed Agenda 2063 in 2013 as a blueprint for turning Africa into the global growth pole and powerhouse of the future.

Africa's Economic Development Paradox

More than sixty years after independence, Africa's structural transformation - the shift of workers from lower to higher productivity employment and intra-sectoral productivity growth - has not progressed as quickly as hoped. Both policymakers and analysts within and outside the continent are genuinely concerned that achieving structural transformation could remain a mirage for many African countries in the absence of bold structural reforms and financing to support implementation of these policies. Why being so pessimistic? Because historical facts tend to support their pessimism. The African Economic Outlook (AEO) 2024 report, released in May by the African Development Bank, reveals that Africa's transformation has been slow and uneven. In countries showing signs of transformation, the process has been characterized by low industrialization and predominantly by employment in low-skill, low-productivity services. The agriculture sector, employing 42% of Africa's workforce, is 60% less productive than the economy-wide average. Consequently, many workers remain trapped in low-productivity, low-wage jobs, unable to escape poverty.

As a result, Africa was the only region of the world where the average real GDP per capita contracted in the 1980s and 1990s, the so-called lost decades.

Africa is off-track in achieving almost all SDG targets by 2030, consistently showing the lowest SDG performance globally since the 2000s (Figure 1). Without intervention, it is predicted that by 2030, nearly 9 out of 10 of the world's extremely poor will be in Africa and under current conditions[1], it could take African countries over a century on average to reach high-income status.

But Africa is a very large, diverse, heterogeneous, region. Some countries have, over the past four decades preceding the COVID-19 pandemic, experienced episodes of growth accelerations, growth spikes and failed take-offs. Cases of consistent good performance include Botswana, Seychelles, and Mauritius, routinely ranked among the top 10 fastest-growing economies globally. African countries have indeed exhibited remarkable resilience amid confounding shocks, and in 2024, 10 countries[2] in Africa are projected to be among the world's top 20 fastest-growing economies, sustaining the trend observed during the past four decades pre-COVID-19.

Importantly, over the past quarter century, thanks to strong economic reforms and macroeconomic stability, enhanced governance, relative peace and improved political environment and, public investments in soft and hard infrastructure, some African countries[3] have managed to transform their economies and recorded economic growth rates above the global average.

The role of finance in fast-tracking Africa's structural transformation

Many factors, both internal and external, could explain the relatively slow progress in structurally transforming African economies. Among them: over-reliance on commodity-led growth, inadequate infrastructure; insufficient pool of skilled workers and low access to affordable finance; weak institutional governance, recurrent conflicts, effects of climate change, tightening of global financial conditions and rising debt vulnerabilities.

While all these factors are equally important and call for urgent actions from policymakers, financing Africa's transformation is a multi-layered overarching challenge that demands special attention and a pragmatic approach to move from billions to trillions. The cost of achieving the SDGs by 2030 in Africa is estimated at about $1.3 trillion annually, equivalent to 42% of Africa's 2023 GDP. Infrastructure needs alone are estimated by the African Development Bank at $181-$221 billion per year over 2023-2030. The climate finance gap is approximately $213.4 billion annually through 2030.

Insufficient domestic resources, compounded by the failure of the global financial architecture to mobilize and at scale, affordable finance for sustainable development, have led many African countries to resort to commercial borrowing on unfavorable terms. This has resulted in increased debt vulnerabilities. Africa's Public and Publicly Guaranteed external debt has nearly tripled since 2010, reaching $656 billion in 2022, accounting for 22.4% of the continent's GDP and exceeding Africa's public revenue-to-GDP ratio of 20.4%. In 2024, African countries are expected to spend around $74 billion on debt service, up from $17 billion in 2010. Out of the projected debt service, $40 billion is owed to private creditors.

Even more concerning, debt service payments now account for about 11% of the continent's total revenues. High debt service is diverting resources from crucial investments in infrastructure, education, and health - all critical for economic transformation and long-term growth. As of April 2024, 20 African countries[4] were either in external debt distress or at high risk of external debt distress.

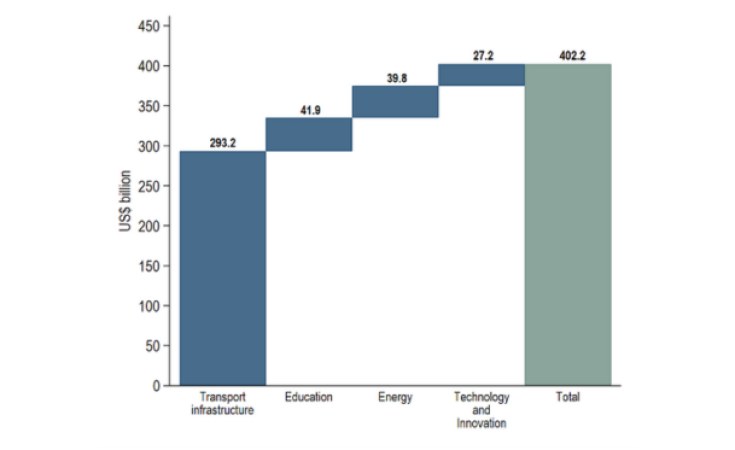

The AEO 2024 report estimates that to accelerate Africa's structural transformation, the continent needs to close an annual financing gap of $402.2 billion (about 13.7% of its projected 2024 GDP) by 2030. Figure 2 shows that transport[5] infrastructure accounts for the largest share of the gap (72.9%), followed by education (10.4%), energy (9.9%), and productivity-enhancing technologies (6.8%). These figures reflect decades of underinvestment in critical areas for development.

The level of financing gap in transport infrastructure reflects the continent's shortfall explained by decades of public underinvestment to upgrade existing road infrastructure or open new roadways, to match the growing population and economic dynamism across the continent. For instance, Africa's median road density is about 12 km per 100 km2, compared with 42.5 km in high-performing developing countries and 136 km in high-income countries. Only about 27% of African roads are paved, far behind the rest of the world (about 49%) and other developing countries (35.4%).

On education, vital for equipping the current and future workforce with the required skillset for structural transformation, African countries' median SDG index score was only 51.5 (out of a maximum of 100) in 2022, while other low-income developing countries reached a median score of 87. In addition, according to World Bank's World Development Indicators, African governments currently spend on average $312 annually per student in primary education, $473 on secondary education, and $2,227 on tertiary education, or about, respectively, 3, 2.3, and 1.1 times lower than high-performing developing countries on SDG 4. On energy, Africa's median SDG 7 index score was 38.8 in 2022, suggesting that a typical African country was 61.2% further away from achieving the best possible outcome on SDG 7 targets. Despite its vast energy potential, electric power consumption per capita in Africa is still the lowest in the world, estimated at 638.4 kilowatt-hours (kWh) in 2021, versus 2,056 kWh in other developing countries. Due to poor energy infrastructure, over 600 million Africans have no access to electricity and this is despite progress in recent years[6]. On productivity-enhancing technology and innovation, the continent lags other regions too. This impedes its ability to either innovate and introduce new products, technologies, and/or services that could support its structural transformation. African countries' average Gross Domestic Expenditure on R&D (GERD) represents about 0.4% of their GDP (against about 1% in the rest of the world) and they spend on average $10.7 per capita on GERD (compared to $403.2 per capita in other regions of the world). Furthermore, the continent displays the lowest concentration of researchers in R&D, with an average of 221 researchers per million people, against 742 researchers in other developing countries.

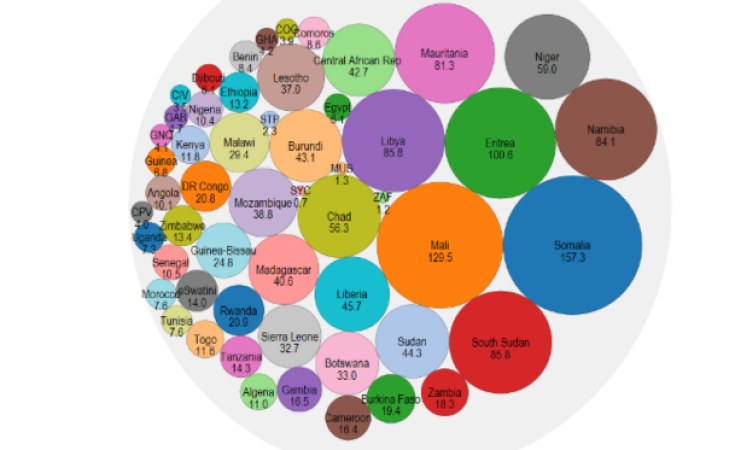

The financing gap varies significantly across countries. The cross-country heterogeneity is mainly explained by differences in current SDG performance related to structural transformation as well as differences in demographics (current and projected population size and composition, land size, and the like) and socioeconomic characteristics (current and projected GDP per capita, and spending on education, infrastructure, and so on). As shown in Figure 3, the estimated annual financing gap represents at least 10 % of 2024's projected GDP in 36 African countries, and in nine of these, at least 50 % of GDP. For such countries, closing the financing gap by 2030 is, therefore, realistically impossible.

A more realistic approach would be to allow for a gradual but steady transformation process over a longer period, aligning with the African Union's Agenda 2063. This would enable countries to mobilize more resources domestically and externally, without jeopardizing debt sustainability.

What next?

Scaling up finance to accelerate Africa's structural transformation should be a key priority for policymakers. While implementing structural reforms is crucial for sustainable growth, success depends on the availability, timeliness, and scale of long-term development financing and enhancing spending efficiency. African countries should therefore, inter alia, focus on: i) scaling up investment to build requisite human capital suited to local realities, circumstances, and development priorities; ii) boosting domestic resource mobilization and improving efficiency of public finance management; iii) creating targeted and streamlined incentives to attract private capital for key transformation sectors; and iv) launching ambitious national infrastructure programs with assured positive returns to attract affordable financing.

The international community should reform the global financial architecture to facilitate African countries' access to long-term, concessional development financing at scale, complementing domestic resources.

By addressing these financing challenges and implementing targeted reforms, Africa can accelerate its structural transformation and move closer to achieving its development goals as espouses in Agenda 2063.

[1] This scenario assumes that real GDP per capita of each African country will grow according to its post-COVID-19 (2022-25) average growth rate as computed by the African Development Bank's Statistics Department.

[2] Niger, Senegal, Libya, Côte d'Ivoire, Ethiopia, Rwanda, Benin, Djibouti, Gambia, and Uganda

[3] Algeria, Comoros, Djibouti, Egypt, eSwatini, Lesotho, Libya, Mauritius, Sao Tome and Principe, Senegal, Seychelles, and Tunisia

[4] Burundi, Cameroon, Central African Republic, Chad, Comoros, Congo, Djibouti, Ethiopia, Gambia, Ghana,

Guinea-Bissau, Kenya, Malawi, Mozambique, São Tomé and Príncipe, Sierra Leone, South Sudan, Sudan, Zambia, and Zimbabwe

[5] Proxied by roads as road transport is the most frequently used means of transporting goods and people across the continent, carrying at least 80 percent of goods and 90 percent of passengers.

[6] For instance, the average share of people with access to electricity increased from about 38 percent in 2000 to about 59 percent in 2022. In 28 African countries, the percent of people with access to electricity has more than doubled between 2000 and 2022, out of which it has increased at least fivefold in 8 countries (Kenya, Lesotho, Mali, Mozambique, Rwanda, Somalia, Tanzania, and Uganda).